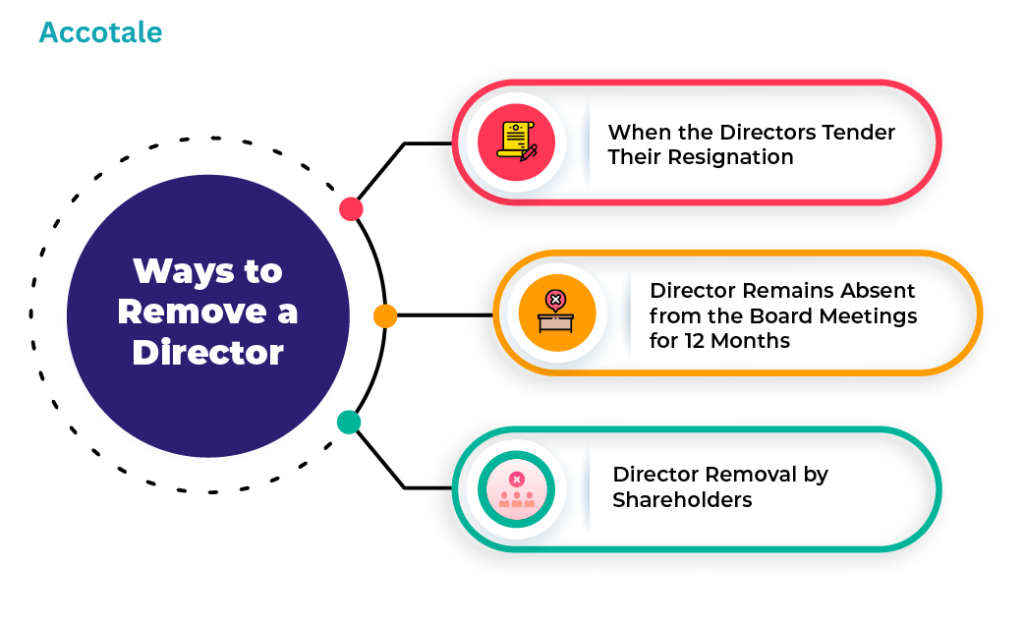

Removal of Director – When the Director Tenders Their Resignation: A director may choose to resign voluntarily from the company. In such cases, the director must submit a written resignation letter to the board of directors. The board will then convene a meeting to accept the resignation and pass a resolution approving it. Once the resignation is approved, the company is required to file Form DIR-12 with the Ministry of Corporate Affairs (MCA) within 30 days, officially recording the resignation. The director must also submit Form DIR-11 to inform the MCA of their resignation.

Process for Resignation:

Director submits a resignation letter.

The board of directors holds a meeting to accept the resignation.

Resolution is passed, and Form DIR-12 is filed with the MCA.

Director submits Form DIR-11 to notify their resignation.

Director Remains Absent from Board Meetings for 12 Months: Under Section 167 of the Companies Act, 2013, if a director is absent from all board meetings held during a continuous period of 12 months, without seeking leave of absence, they may be disqualified and automatically vacate their position as a director. This removal does not require shareholder approval. The company must record the absence and file the necessary forms with the MCA to complete the removal.

Process for Absenteeism Removal:

Director misses all board meetings for 12 consecutive months.

Board records the absence and notes the automatic vacation of office.

Form DIR-12 is filed with the MCA to update the company’s records.

Removal of Director by Shareholders: Shareholders have the right to remove a director before the expiration of their tenure by passing an ordinary resolution at a general meeting. This can be done in accordance with Section 169 of the Companies Act, 2013. The company must issue a special notice of the proposed removal to the shareholders, and the director in question must be given an opportunity to present their case before the resolution is passed. Once approved, the company must file Form DIR-12 with the MCA to complete the removal process.

Process for Shareholder-Initiated Removal:

A special notice is issued to shareholders regarding the proposed removal.

General meeting is convened, and the director is given an opportunity to defend themselves.

Shareholders vote on the removal, and if passed, the director is removed.

Form DIR-12 is filed with the MCA to finalize the removal.

")